ICCT zero-emission truck market report: steady growth in the light and medium segments in H1, 2025

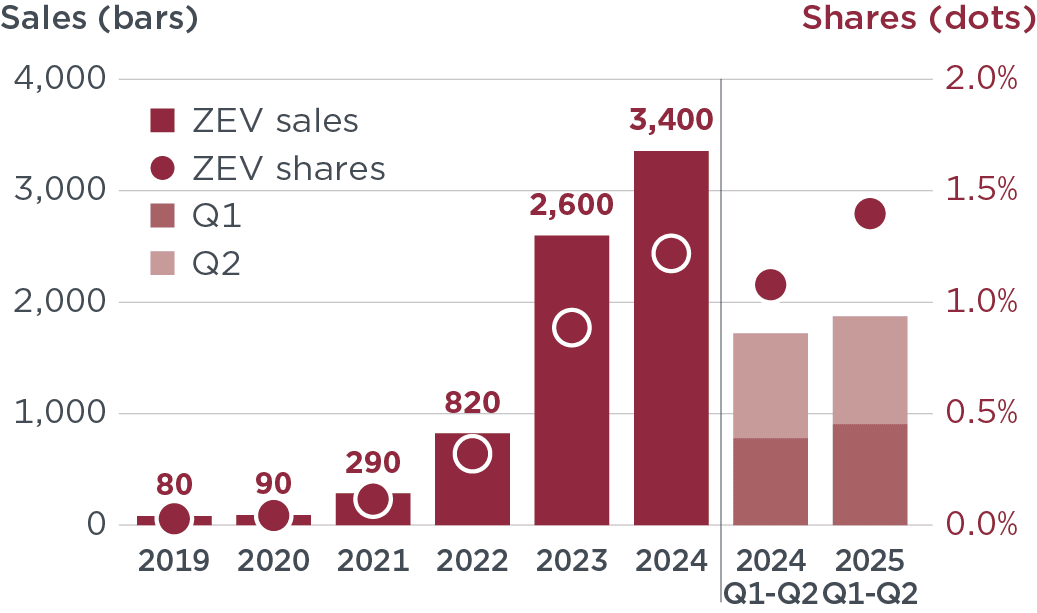

New zero-emission truck and bus registrations rose by 40%, from 7,100 to 10,000, in the first half of the year. More into details, shares of ZE light and medium trucks more than doubled from 9% to 19% in Q1–Q2 2025 compared with the same period in 2024, with 4,000 vehicles sold, up from 2,400. Growth in the sales of ZE heavy trucks was less pronounced, with sales in Q1–Q2 2025 broadly equal to the same period in 2024 but with shares reaching 1.4%, up from 1.1% in Q1–Q2 2024.

All the infographics are provided by the ICCT

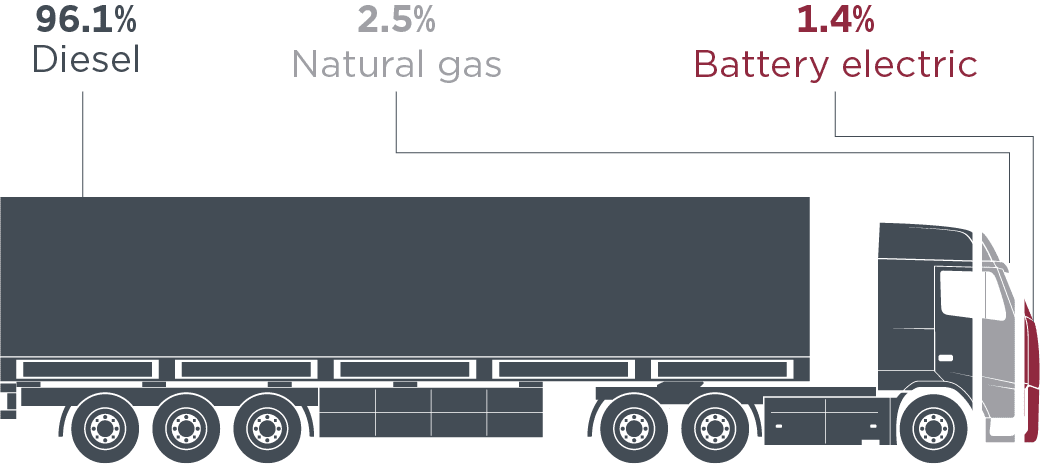

According to the awaited zero-emission truck market report issued by ICCT (here’s the full report, available on their website), the light and medium segments experienced steady growth compared to H1, 2024. On the other hand, the situation is quite the same in the heavy-duty truck segment (over 12 tonnes), still struggling and not advancing.

New zero-emission truck and bus registrations rose by 40%, from 7,100 to 10,000, in the first half of the year. More into details, shares of ZE light and medium trucks more than doubled from 9% to 19% in Q1–Q2 2025 compared with the same period in 2024, with 4,000 vehicles sold, up from 2,400. Growth in the sales of ZE heavy trucks was less pronounced, with sales in Q1–Q2 2025 broadly equal to the same period in 2024 but with shares reaching 1.4%, up from 1.1% in Q1–Q2 2024.

The ICCT underlines that the renown CO2 reduction target of 15% for heavy trucks will first apply in Q3 2025, which may spur further growth in the sector in the second half of the year. CO2 targets will not apply to light and medium trucks or to buses and coaches until 2030.

Zero-emission truck market: heavy trucks for brand and country

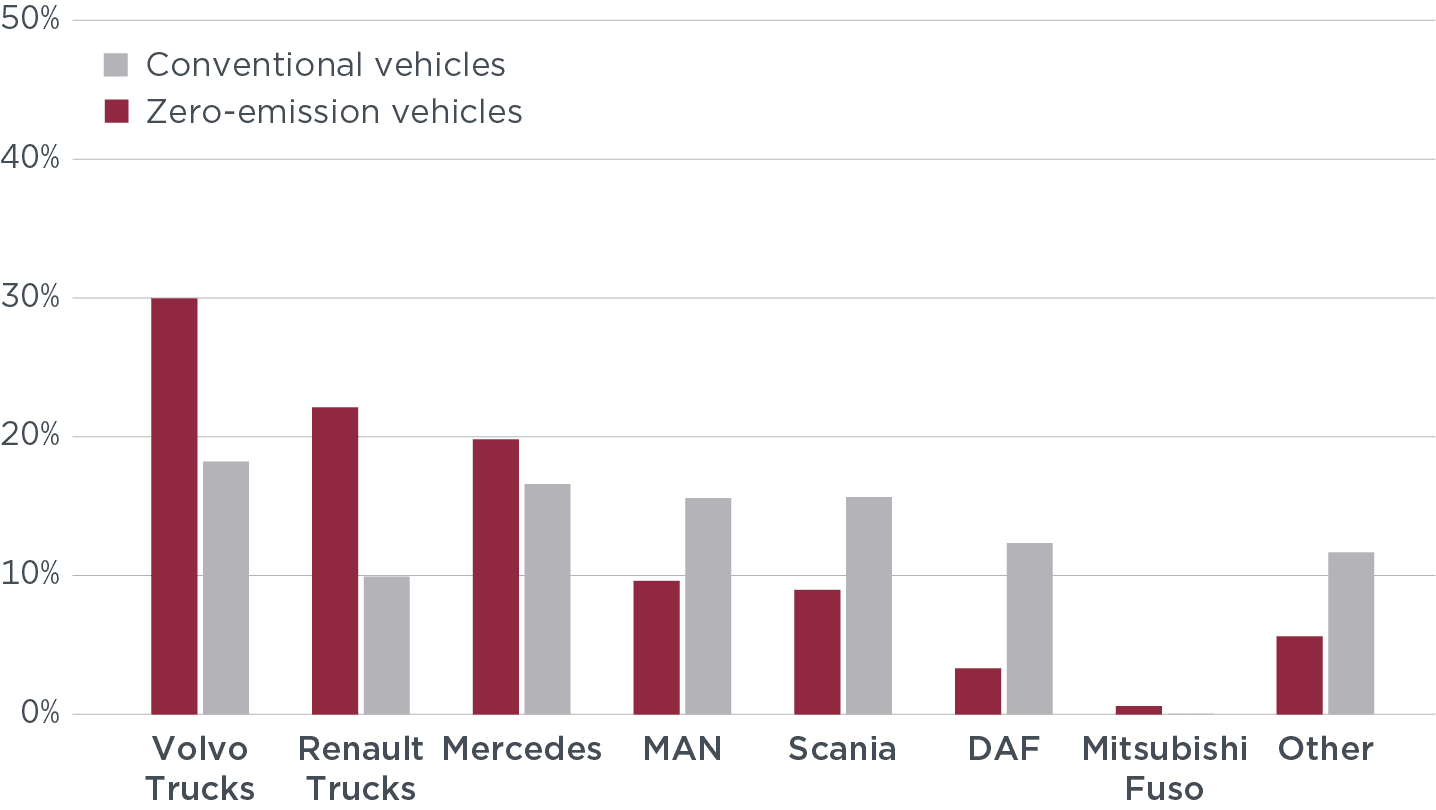

In the heavy truck segment, out of 134,000 heavy trucks sold, 1,900 were ZE HDVs. Talking about truck makers, Volvo and Renault, two brands of the Volvo Group, continue to dominate the ZE market by volume, comprising a combined share of more than 50% of all ZE heavy truck sales in Q1–Q2 2025, albeit down from a 66% share in Q1–Q2 2024. Mercedes and MAN both increased their sales shares over this period. MAN’s share of all ZE heavy trucks sold rose from 1% in Q1–Q2 2024 to 10% in Q1–Q2 2025, owing largely to continued sales of its eTGX model. Mercedes made up just under 20% of ZE heavy truck sales in Q1–Q2 2025, largely driven by increasing sales of its eActros. Iveco sold just 7 ZE heavy trucks in Q1–Q2 2025.

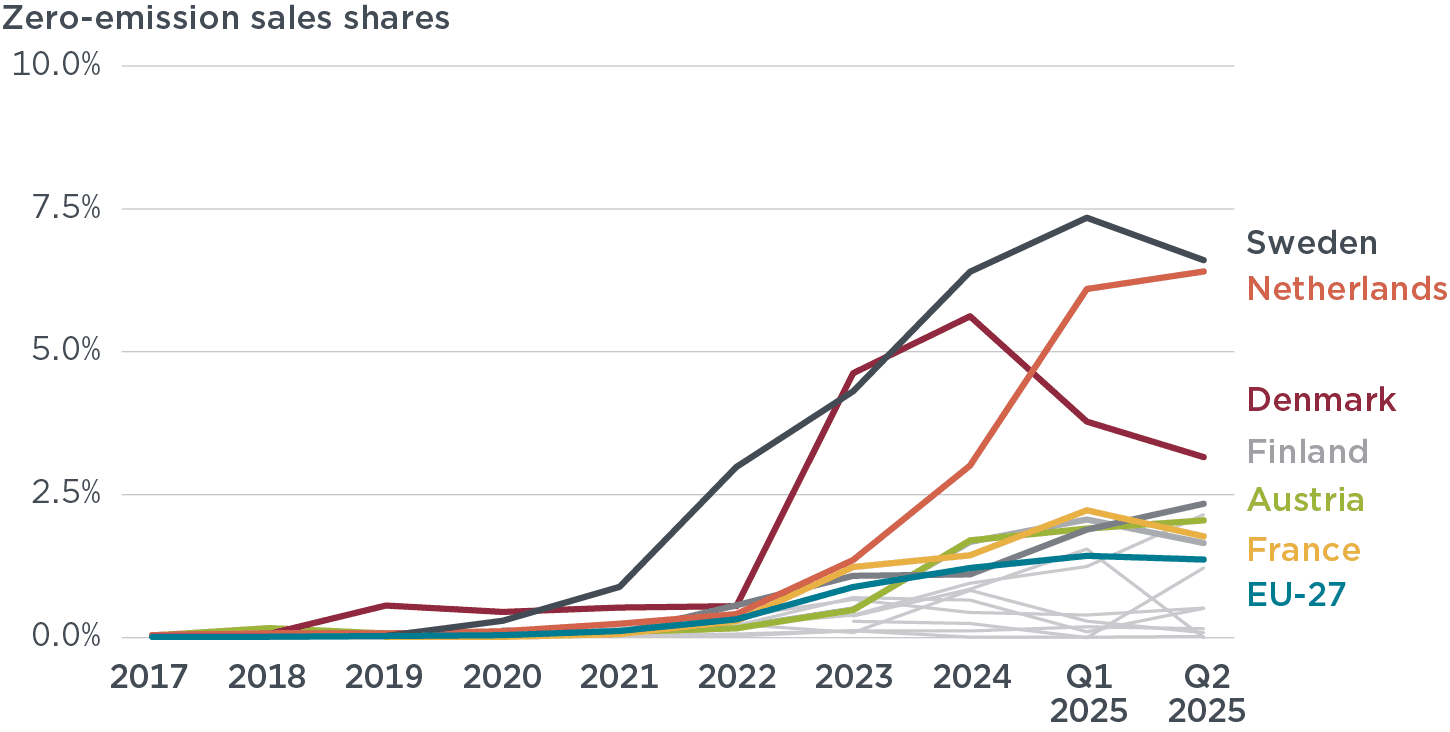

Despite market contractions, Germany remains the largest market for ZE heavy truck sales by volume in Q1–Q2 2025 (580 sales, 1.8% share), closely followed by France (410 sales, 2.0% share). While most countries had a ZE sales share below 2.5% of all sales, shares in Sweden and the Netherlands far exceeded the EU-27 average, reaching 7.0% (180 vehicles) and 6.3% (310 vehicles), respectively, in Q1–Q2 2025.

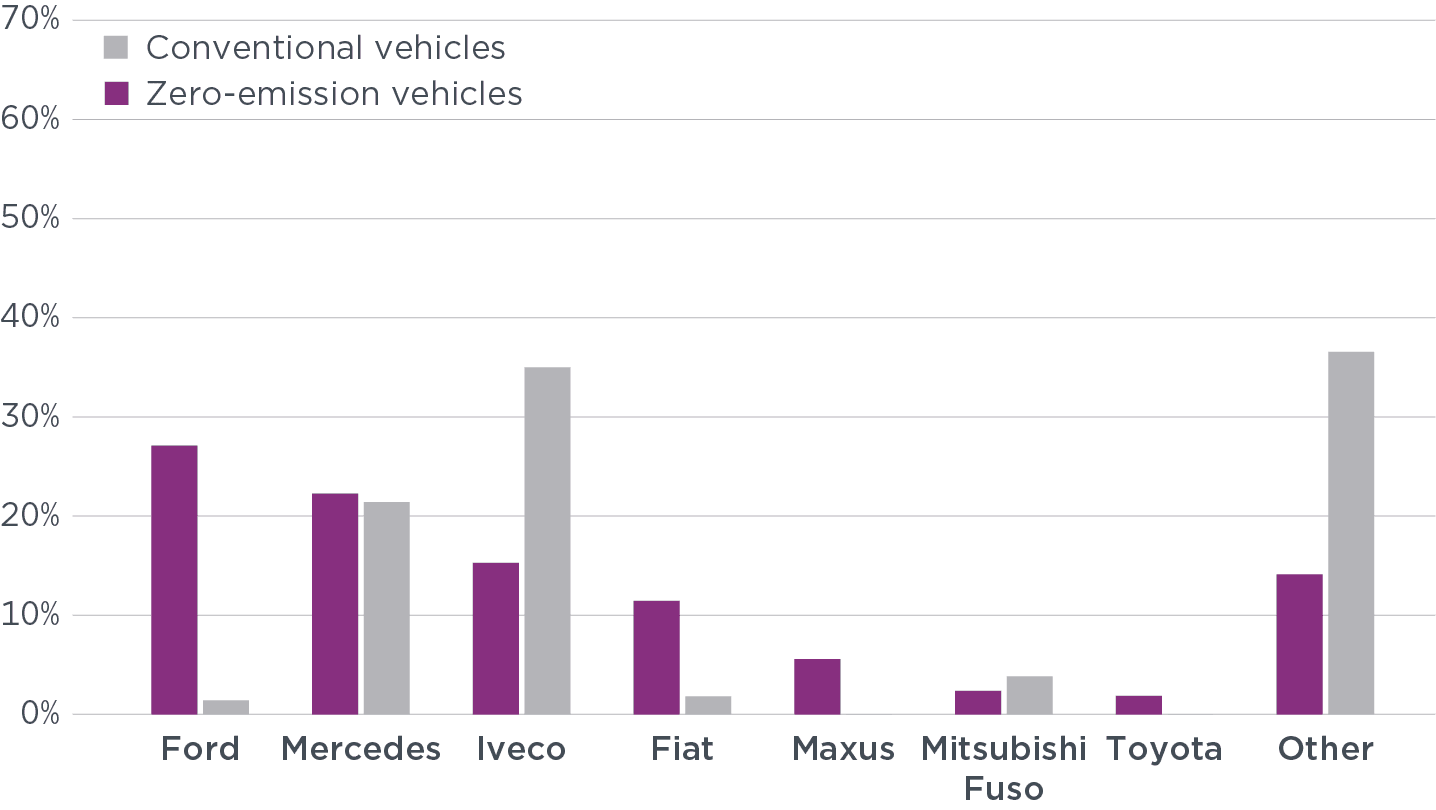

Light and medium trucks (3.5 to 12 tonnes)

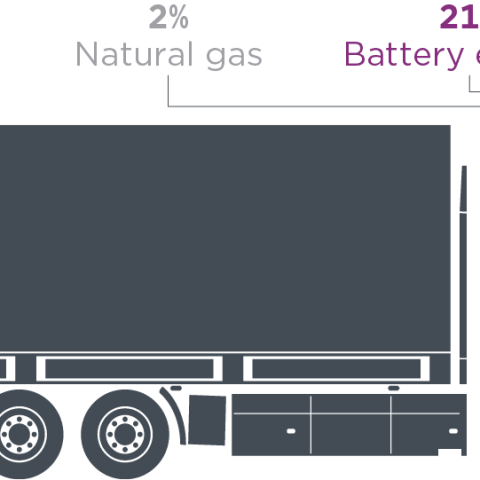

In the light and medium truck sector (from 3.5 to 12 tonnes), of the 21,000 vehicles sold, 4,000 were ZE HDVs, making up 19% of the segment’s sales. This marked a more than doubling in shares over Q1–Q2 2024, in which 9% (or 2,400) of trucks sold were ZE.

Most ZE light and medium trucks were comprised of just four models: Ford’s E-Transit (25% of all ZE light and medium truck sales in Q1–Q2 2025), Mercedes’ eSprinter (22%), Iveco’s eDaily (15%), and Fiat’s E-Ducato (11%). The sale of ZE light and medium trucks has been concentrated in the 3.5 t–5 t weight range, which comprises nearly 70% of all ZE sales but just 15% of conventional vehicle sales.

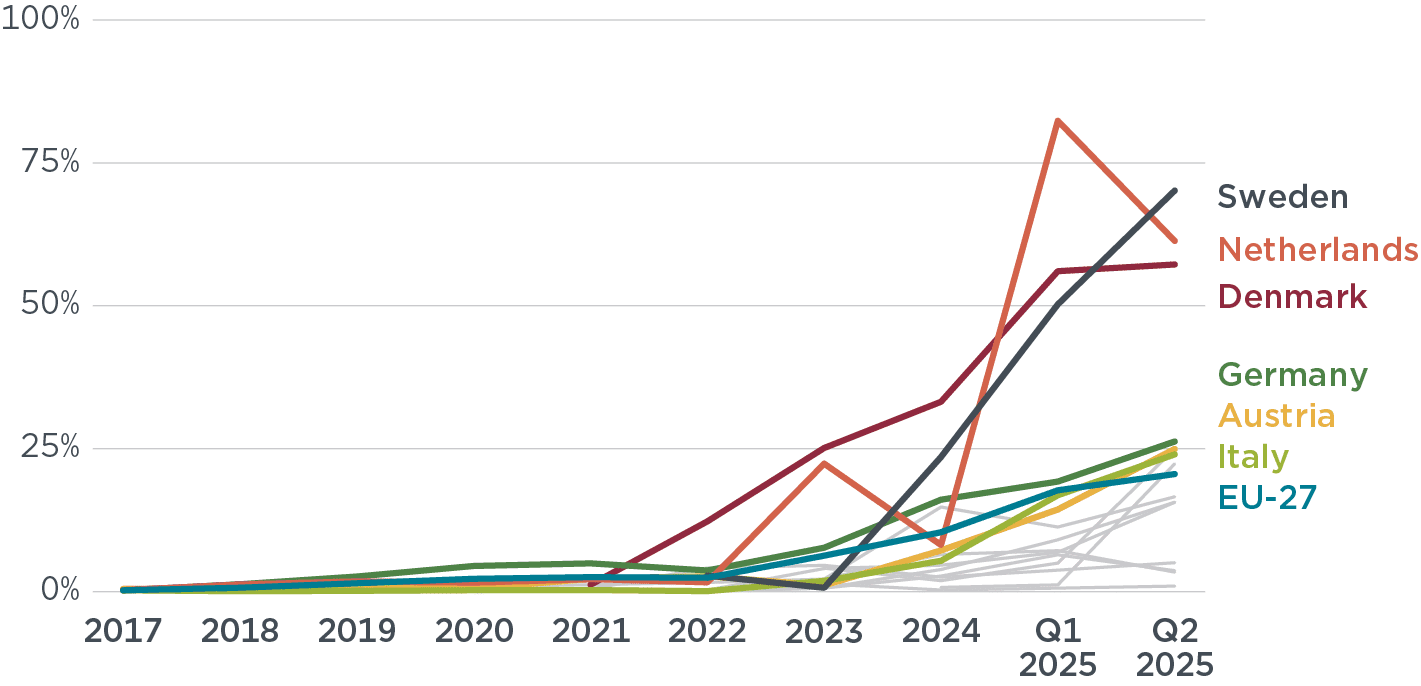

The sales shares of ZE light and medium trucks surpassed 50% in the Netherlands, Denmark, and Sweden in Q1–Q2 2025. Sweden has shown particularly rapid growth, with ZE shares rising from <1% in 2023 to 72% in Q2 2025. Possibly driving this growth was the subsidy scheme launched in early 2024 that funded up to 25% of the cost of an electric truck, rising to 60% in the case of small enterprises.